A version of this post originally appeared on the StartupYard blog in January 2016. As a new group of Startups joins us in the next few weeks for StartupYard Batch 10, we thought we’d dive back into a very important topic for them: How do the smartest startups engage their mentors?

But first: why do some of even the most successful startup founders continue to seek mentorship?

Mergim Cahani (right), CEO of Gjirafa, one of StartupYard’s most successful alumni, is an avid startup mentor himself.

Founders have to balance mentorship with the day-to-day responsibilities of their companies. But sometimes founders approach mentorship as a kind of “detour” from their normal operations- something they can get through before “getting back to work.”

This is the wrong approach. Having worked with scores of startups myself, as a mentor, investor, and at StartupYard, I can comfortably say that those who engage with mentors most, get the most productive work done. Those who engage least, are generally the most likely to waste precious time.

How can that be? Well, simply put, the first line of defense against the dumbest, most avoidable mistakes, are mentors who have made those mistakes themselves. I’ve seen this happen: a startup decides they’re going to try a certain thing, and it’s going to take X amount of work (often a lot of work). They mention it to a mentor, who forcefully advises that they not do it. The mentor tried it themselves, and failed.

Now this startup has 2 options: proceed knowing how and why the mentor failed, or change direction to avoid the same problems. Either way, an hour-long discussion with a mentor will probably have saved time and money, simply by raising awareness. I have seen 20 minute conversations with mentors save literally months of pain and struggle for startup founders.

Recently, one of our founders reached out to a handful of mentors for information on an investor who was very close to signing on as an Angel. The reaction was swift, and saved the founder from making a very serious mistake. The investor turned out to have a bad reputation, and was a huge risk. As a result, mentors scrambled to suggest alternatives and offer help securing the funds elsewhere. That is what engaged mentors can do for startups.

There’s a tendency, particularly among startups that haven’t had enough challenging interactions with outsiders, to paper-over issues that the founders prefer not to think about. Often there “just isn’t enough data,” to prove or disprove the founders’ theories about the market.

Conveniently, “lack of data,” or “need for further study,” can serve as an excuse for not making decisions. That’s one of the main reasons startups fail – refusing to make a decision before it’s too late.

We like to focus on things we can control, and things we have a hard time working out appear to be outside of that sphere, so we are more likely to ignore them, or hand-wave their importance away.

Founders sometimes long to go back into “builder mode,” and focus solely on executing all the advice they’ve been given. And they do usually still have a lot of building to do. But one common mistake -something we see every single year- is that startups will treat mentors as the source of individual ideas or advice, but not as a wellspring of continuing support and continual challenges.

The truth is that a great mentor will continually put a brake on your worst habits as a company. They will be a steadfast advocate of a certain point of view- hopefully one that differs from your own, and makes you better at answering tough questions. But you have to bring them in.

I can’t say how many times great mentors, who have had big impacts on the teams they have worked with, have come to me asking for updates about those teams. These mentors would probably be flattered to hear what an effect they’ve had on their favorite startups, but the startups often won’t tell them. And the mentors, not knowing whether they’ve been listened to, don’t press the issue either.

Mentors need care and feeding. They need love. Like in any relationship, this requires effort on both sides.

But time and again, mentors who are ready to offer support, further contacts, and more, are simply left with the impression that the startup isn’t doing anything, much less anything they recommended or hoped the startup would try.

Mentors who aren’t engaged with a startup’s activities won’t mention them to colleagues and friends. They won’t brag about progress they don’t know about, and they won’t think of the startup the next time they meet someone who would be an interesting contact for the founders.

This isn’t terribly complicated stuff. Many founders fear at first that “spamming” or “networking,” is the act of the desperate and the unloved. If their ideas are brilliant and their products genius, then surely success will simply find them. Or so the thinking goes.

Alas, that’s a powerful Silicon Valley myth. And believe me: it doesn’t apply to you. Engaging mentors is just like engaging customers: even if you’re Steve Jobs or Elon Musk, you still need to be challenged and questioned. You still need support.

As always, there are a few simple best practices to follow.

Two of StartupYard’s best Alumni, Gjirafa and TeskaLabs, provide regular “Mentor Update” newsletters. These letters can follow a few different formats, but the important things are these: be consistent in format, and update regularly. Ales Teska, TeskaLab’s founder, sends a monthly update to all mentors and advisors.

In the email, he has 4 major sections. Here they are with explanations of the purpose of each:

Here you give a personal account of how things are going. You can mention personal news, or news about the team, offices, team activities, and other minutiae. This is a good place to tell small stories that may be interesting to your mentors, and will help them to feel they know you better. Did a member of the team become a parent? Tell it here. Did you travel to Dubai on business? Give a quick account of the trip.

This is one section which I love about Ales’s emails. I always scroll down to the “ask” section, and read it right away. Here, Ales comes up with a new request for his mentors every single time. It can be something simple like: “we really need a good coffee provider for the office,” to something bigger, like “we are looking for an all-star security-focused salesman with 10 years experience.”

Whatever it is, he engages his mentors to answer the questions they know, by replying directly to the email. This way, he can gauge who is reading the emails, and he can very quickly get great answers to important questions or requests.

Audience engagement happens on many levels. Not everything engages every mentor all the time, and that’s important to keep in mind. A simple question can start an important conversation. You don’t know what a mentor has to offer you until you find the right way to ask for their help.

Here, Ales usually shares any good news he has about the company. This section is invaluable, because it reminds mentors that the company is moving forward, and making gains. A win can be anything positive. You can say that a win was hiring a great new developer, or finally getting the perfect offices. Or it can be an investment or a new client contact. These show mentors that you are working hard, and that you are making progress and experiencing some form of traction.

You’d be surprised how many mentors simply assume that a startup that isn’t talking about any successes, must have already failed. StartupLand in can be like Hollywood that way: if you haven’t seen someone’s name on the billboards lately, it means they’ve washed out.

The fact might be that you’re quietly doing great business, but see what happens when someone asks about you to a mentor who hasn’t heard anything in 6 months. “Those guys? I don’t know… I guess they aren’t doing much, I haven’t heard from them in a while.” There’s no good reason for that conversation to happen that way.

Here Ales shares a consistent set of Key Performance Indicators. In his case, it is about the company’s sales pipeline, but for other companies, it might be slightly different items, such as “time on site,” or “number of daily logins,” or “mentions in media.” Whatever KPIs are most important to your growth as a company, these should be shared proactively with your mentors.

If the news isn’t positive, then explain why. You can also have a little fun with this, and include silly KPIs like: “pizza consumed,” or “bugs found.” This exercise shows mentors that you are moving forward, and gives them a reliable and repeatable overview of what you’re experiencing in any given week.

I heard one mentor complaining not long ago about these types of emails. “The KPIs don’t change that much, it’s always the same thing.” But he was thinking about the startup in question. The fact that the KPIs hadn’t changed might be a bad sign to the mentor, but probably the absence of any contact would be worse. At least in this case, the mentor might care enough to reach out and ask what’s going on.

Mentors aren’t mushrooms. They don’t do well in the dark. Once you’ve identified your most engaged mentors, you need to put in as much effort in growing your relationship as you expect to get back from them.

How can you grow a relationship with a mentor? Start by identifying what the mentor wishes to accomplish in their career, in their life, or in their work with you. Do they want to move up the career path? Do they want to do something good for the human race? Do they just want to feel needed or important?

A person’s motivations for mentorship can work to your advantage. Try and help them achieve their goals, so that they can help you achieve yours.

Does a mentor want his or her boss’s job? Feed them information that will help them get ahead of colleagues and stand out. Mention them in your PR, or on your blog to enhance their visibility.

Does the mentor want to be a humanitarian? Show them the positive effects they’ve had by sending them a letter, or inviting them to a dinner.

Does the founder yearn to be needed? Include his/her name in your newsletter and highlight their importance to your startup. These things are all easy to do, and can be the difference between a mentor choosing to help you, and finding other things to do with their busy schedules.

Last week in Prague, the famous inventor, sci-fi author and speaker Ramez Naam gave a talk about one of our favorite topics: Exponential Innovation, under the auspices of DirectPeople. Ramez Naam is not only an award winning author, he is also a veteran of Microsoft, the holder of 19 separate patents, and the founder of Apex Nanotechnologies, which is the first company to create software tools for molecular design.

The partnership is fitting, as DirectPeople works with companies and startups to realize innovative new projects, building teams around new ideas and executing them for banks, energy companies, and telcos, as well as smaller firms. (Full disclosure: Petr Sidlo, CEO at DirectPeople, is our mentor, and Phillip Staehelin their Innovation Evangelist is our mentor and investor.)

The talk centered around an introduction to exponential thinking, much like those we have written before. What really stood out from the talk however, was Naam’s particular attention to the reasoning that so often fails to predict radical changes in the business and technology landscapes. As important as the exponential innovation framework is, we must put it in context with the logic that has failed to match it over and over again.

The talk was a long one, so I’ve chosen to focus on 3 key errors that perpetually lead industries as well as individuals to dramatically underestimate the effects of innovation over long periods. As Naam pointed out in his talk,

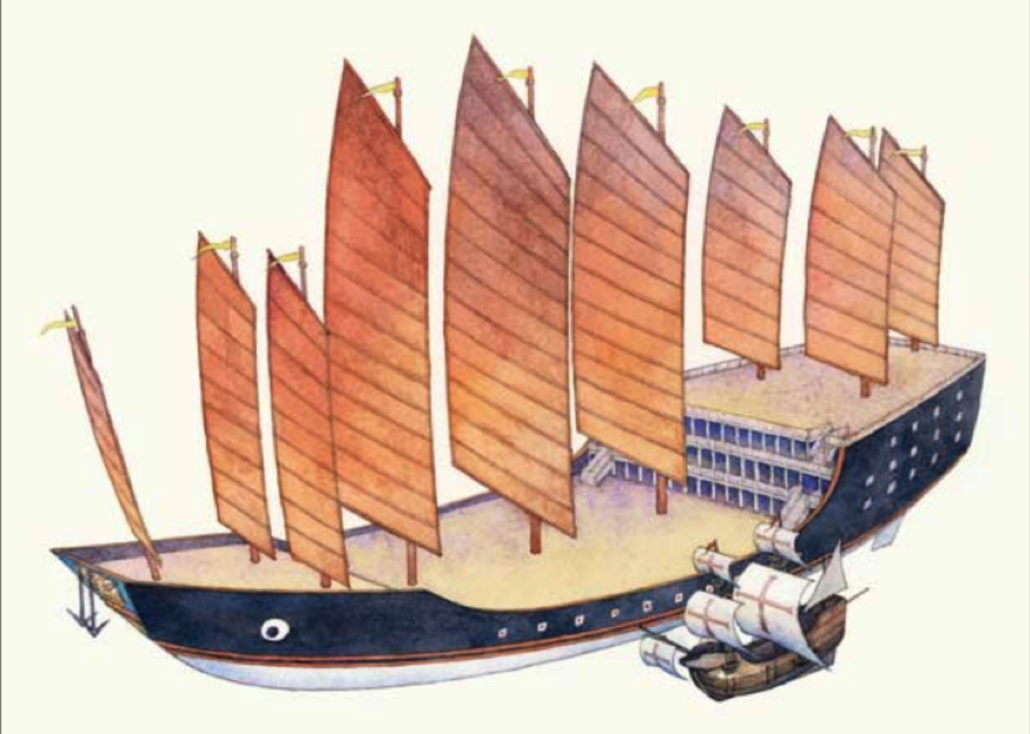

One of the key analogies Naam used was the broad history of world empires beginning around A.D. 1400-1500, with two key events: the European discovery of America by Columbus’s fleet, and the exploration of South Asia by Zheng He of China.

To scale: the flagship of the Chinese fleet of 1400 (larger), and the Santa Maria (smaller).

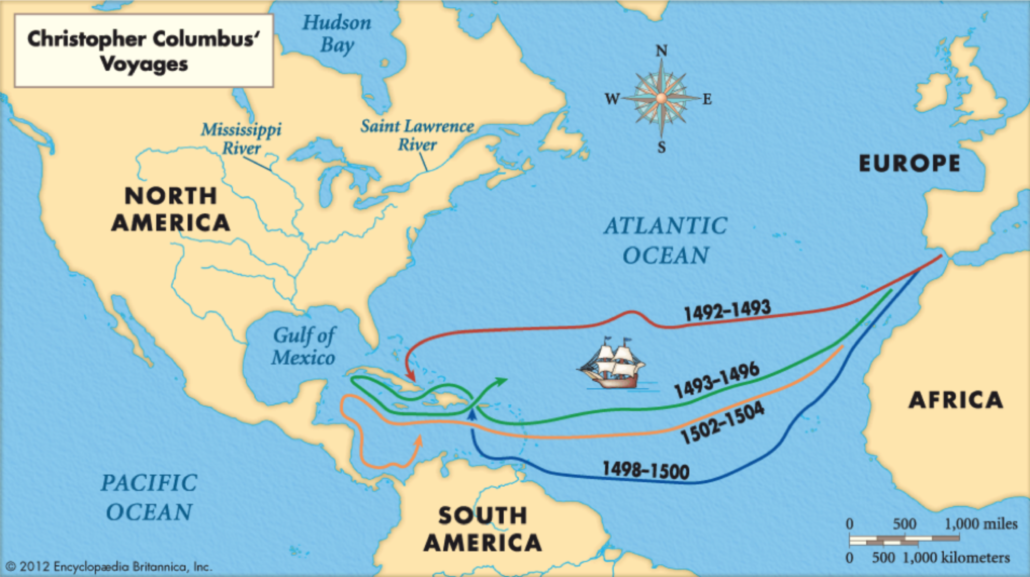

Though the two events bear remarkable similarity in their timing and boldness, there the similarities end. Columbus’s voyage was an accidental success. Attempting to circumnavigate the globe with too little food and resources, his fleet was saved by the accidental discovery of Cuba, a fraction of the total distance to his actual target, East Asia and India.

Zheng He, on the other hand, commanded the most technologically advanced navy in the world. His ships made Columbus’s tramp fleet of the Nina, Pinta, and Santa Maria look like bath toys in comparison. His expedition was well planned and financed, took much less risk, and made much more important near term discoveries for China in the form of large potential trading partners.

Yet, Columbus’s voyage set off an imperial age in Europe that lasted for nearly 5 centuries, and saw the colonization and Europeanization of most of the world. Zheng He’s 25 year exploration of South Asia and East Africa ended in the burning of his fleet, and the closing of China from the outside world for another 4 centuries.

Why these two vastly dissimilar outcomes? Moreover, why did the results of a well funded, professional, and government backed expedition (that of Zheng He), result in nothing of significance, when the poorly funded, badly planned expedition of Columbus ended in Spain’s domination of South America for hundreds of years, and Britain’s eventual domination of half the world?

Top Down V. Bottom Up:

There is one key differentiator: China’s exploration of the known world was a top-down affair, instigated by the emperor, and carried out on behalf of China’s leadership. It was essentially a government program/ Meanwhile, Columbus’s voyage was backed by Queen Isabella of Spain (after other monarchs turned it down), but she served as little more than a financier. The project was from the beginning a bottom-up effort by Columbus, and would have been doomed to failure and the death of the entire fleet, if not for America conveniently sitting between Europe and Asia. Columbus lucked into a discovery that eventually made him rich and famous. He took the key risk (with his life), and so he also owned his share of the rewards.

Again, Naam directs our attention to the effects that leadership structure had on the resulting discoveries. While Zheng He returned to China a hero, his discoveries and fleet were the property of the Emperor, who chose simply to dismantle them, rather than to take the risk of engaging with foreign trade and potentially coming into conflict with foreign powers. To China, the fleet represented a cost and risk that was evaluated based on the status quo. Since the voyage proved that China was the most powerful nation on Earth, the Chinese saw no more reason to engage with the outside world and risk their already safe position.

Stability Becomes a Liability

Columbus was in a weaker position from the beginning. So why did he win? Naam argues that it is because of the inherently competitive nature of European politics at the time. While China was unified under the Ming Dynasty for 3 centuries (from 1368-1644), Europe’s political landscape was inherently unstable, and composed of hundreds of individual state-like entities, with nobles fighting for position and consolidating control of their regions.

It was that instability which made it difficult for any one government to back Columbus, and it was the need for a competitive advantage that drove Isabella, who had only just united Spain under one ruler, to fund him. The price of not having state control of the expedition was that Columbus himself (along with the explorers and conquistadors who followed), personally profited from their efforts. A traditional of entrepreneurial exploration was established because Europe could not afford to publicly fund it.

Thus, Columbus’s voyages were highly disruptive to the established order because Europeans were desperate to gain competitive advantages over neighbors. Meanwhile China, the strongest nation in the world at the time, had no such need. In fact, quite the opposite, as opening itself to trade only served to destabilize China when it eventually did realize it could no longer afford to remain closed. It was finally Britain that forced the opening of China and established Hong Kong as its trading colony in the late 19th century.

One does not have to look too hard here to recognize the tech startup and the modern corporation. Stability for its own sake can turn to a liability over time, as hungry younger competitors adapt too quickly and are too numerous to be stopped.

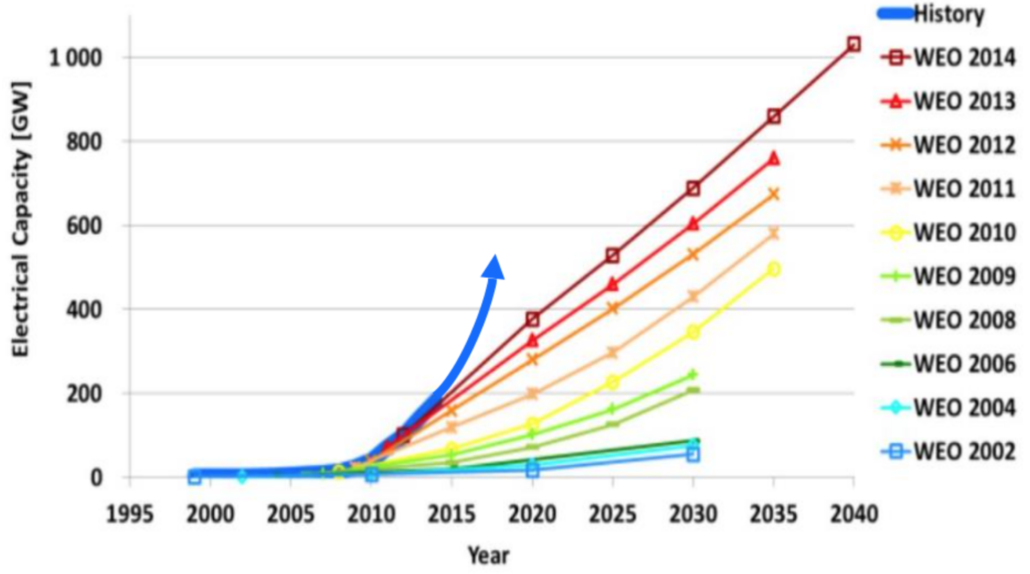

Naam spent a lot of time covering the ways in which exponential innovations deceive people into seeing them as always just about to slow down. This is because the fundamental drivers of innovation are often mistaken as being the same as they were before the exponential growth curve took effect. He shared this graph, for example:

The graph shows a classic exponential curve in the electrical capacity of solar power from roughly 1998 to 2014, along with the World Energy Organization predictions of future growth. As is plain to see, every single prediction over 12 years shows static growth, but realigned from the new actual baseline in any given year. Every prediction is not only wrong, it’s wrong in exactly the same way.

Why would that continue to happen for 16+ years in a row? Surely someone at the WEO might notice it happening and try to figure out why?

Exponential Innovations are on a broad front:

Naam provides a partial answer in this blog post on the topic. He points out that predictions typically take a snapshot of the industry at the present moment, and extrapolate expected advances based on what appear to be limitations to growth that are non-surmountable without a step change in the technology or the underlying economy.

This works most of the time, because most of the time the specific conditions for exponential innovation aren’t met. Namely: that advances in different aspects of a technology produce feedback to affect growth in other areas. Innovation is happening on a “broad front.”

In this particular case, the reason the predictions are wrong is not because their underlying assumptions are inaccurate, but because they are about the wrong things.

For example, predictions of the slowed growth of solar energy may point to theoretical limitations in the materials being used to make solar panels. Indeed, solar panel efficiency is not growing as fast as it did in the past. Instead, as Naam points out in his post, the manufacturing methods are improving faster instead, which is compensating for the diminishing returns of material science advances.

This effect repeats itself over and over again. If it isn’t manufacturing, it’s software. If it isn’t software, it’s infrastructure changes. If it isn’t that, it’s changes in the consumer business model that accelerate growth. The growth in total wattage keeps going up exponentially because all these advances are driving each other forward at once.

On the last point about innovation around the economic models of new technologies, Ramez Naam took special care. He argues that exponentiality of innovation depends on the technology’s ability to be democratized over time.

In fact, in reference to solar power, he used Nuclear energy as a counter-example. Despite the enormous efficiency and effectiveness of modern nuclear power, it is failing to keep up with solar energy in the growth of its footprint. In fact it is declining. Predictions by Isaac Asimov and many others about a nuclear future in which atomic cores power watches and handheld computers, or even body implants, are now severely dated.

Why is that? Naam argues that it is because Nuclear power is difficult or impossible to democratize. Simply because of how it works, and its ability to be weaponized, atomic power must remain under the control of governments. This means that the core technologies involved with nuclear power have fewer chances to influence other areas of technology growth, and vice versa. Nuclear grows in a kind of parallel, where advances don’t greatly benefit other technology areas, and so other technologies don’t arise to create demand for new innovations.

Nuclear is not doomed because the technology doesn’t work, but rather because it can’t be enmeshed with other businesses and technologies. Like China’s great navy in 1400, nuclear is a state operation: it can’t be democratized because it is too dangerous.

If we go back to the previous example of Columbus and Zheng He, we see that a classical prediction would state that the Chinese technical superiority would allow them to predominate or to catch up quickly with the west. But what actually ended up happening was that the west innovated around the business model of exploration first, and the attractive monetary incentives led a revolution in technology that profited from the scalable finance model that colonization had created.

Consider the fate of nuclear vs. solar power in that context. Nuclear is far and away more complex technology. The only problem is that might not matter. The innovation that advances on a broad front and permeates society will win out.

By the time the British Empire came into direct conflict with China, it was the English who had developed the use of colonies as markets for their own goods, rather than a source of resources for the use of their own governments or ruling classes. Thus the English could afford conflict with China, because colonization was immediately profitable to those involved, rather than to established players only.

Indeed, this innovation is what made the American revolution the opposite of a disaster for England. Because England had repurposed itself as the workshop of the world, the growth of American power and economic strength helped the British empire to finance itself through trade with America. Britain had innovated away from the old definition of an Empire through mercantilism and trade. The state did not have to directly fund exploration and colonization because it shared the profits with the colonies themselves.

The English democratized economics itself. That was the innovation. It was one China still struggles to match.

So too with solar energy: solar power can afford to compete directly with traditional sources because it brings the benefits of the new technology closer to those who will profit from it. Even when solar was not at cost-parity with traditional fossil fuels (which is no longer true), it was cost effective for those who adopted it, because they saw the benefits personally, and over the long term. The risk of adoption had an appropriate reward.

Unlike with nuclear power or coal, which require long-term up-front investments far from view of those who pay for them, solar is a source of energy consumers and businesses can own themselves. This means they’re increasingly likely to invest in it, and to see less risk in doing so. The technology is thus democratized, and suddenly it can be the basis for knew, previously unimagined products or businesses.

The innovation can be in the business model this makes possible: not always in the technologies that underwrite the growth. Exponential Innovation shifts streams and goes around obstacles, rather than charting a straight line in one area. Thus predictions from the WEO may accurately represent technological limitations, but still fail to predict growth because they are using an outdated economic model.

On the one hand, if predicting the future were as easy as a new mental framework, then everyone would be doing it already. Yet on the other, we can avoid making the same wrong predictions over and over by paying attention to what causes an exponential growth cycle in a particular industry or technology.

One of the key takeaways for me from Ramez Naam’s talk was that exponential change occurs primarily where there are multiple axes of advance being explored at once. If one hits a wall, another can cause the technology’s adoption to grow any way. What is inherent in an exponential growth model is that growth never depends on one particular characteristic of a technology, but rather on the overwhelming incentives it creates. People want it to grow, and so it does. That was the fundamental insight of Moore’s Law decades ago. Limitations we recognize as crucial today can become meaningless tomorrow, because the incentive structure for innovation is self-feeding.

Singularity University uses a framework called the 6 “D”s (also used by Ramez Naam), namely: Digitized, Deceptive, Disruptive, Demonetized, Dematerialized, and Democratized. In broad strokes, they argue that an organization or industry becomes exponential when the following conditions occur:

Given these conditions, a technology may reach an exponential growth curve, and if we recognize a technology that begins to fall into this particular virtuous cycle, we must closely examine whether or not traditional predictive frameworks of the future remain useful.

Yesterday we received an email that I can only describe as an “hysterical screed” from a disappointed startup founder who felt that his ideas had been “stolen” by the likes of Y-Combinator some years ago. The email included links to an elaborate set of documentation including YouTube videos that compared two products that sort of, kind of do similar things.

Note, neither the message nor the documentation ever contended that any actual intellectual property, such as code or wireframes, had been stolen. Only the ideas behind them.

What was more arresting was the content of the email, which verged into conspiracy theorism and fantasy.

We get our fair share of weird mail. Investors seem to attract people who combine sad desperation with megalomania. Some just want money. Still when Cedric sent me this email saying: “Maybe a blog post?” I responded: “Hell yes.”

I am not posting this to defend the good name of startup accelerators worldwide, nor to defend StartupYard against such an accusation. I’m also not posting it to ridicule this person, because I am sure their problems are deeper than professional disappointment.

Rather I’m hoping to show startup founders how insidious and destructive the concept of “Idea Ownership,” really is, and why they ought to think very hard before making accusations of IP theft. Again, not because these accusations are particularly damaging to those who are accused, but because they are quite damaging to those who make the accusations, and to the many people out there who have great ideas to share.

The general gist of the supposed conspiracy was summed up in a few bullet points I will paraphrase (though I won’t give free publicity to the author):

Please understand, I am not exaggerating. It was taken as a given that finding the best ideas out of thousands of applications would lead to multi-hundred million dollar exits.

If only that were the case! How easy life would be for accelerators like StartupYard. Not to mention those lucky startups we would give the stolen ideas to.

But sadly no, it just does not work that way. Your ideas are pretty much worthless. Let me explain why that is:

The central plank of this theory is that investors and VCs are out digging through your garbage and listening to your phone calls trying to steal your ideas.

We’re not. You know why? Because we’ve heard them already. Yes, even that one. A typical VC is pitched a couple of hundred ideas a year. I see around 400-500 a year. Every year. It gets so that when I hear a pitch these days, I sometimes struggle to remember whether I have already met the founder who is pitching, because I know about the idea already.

What was funny to me about this particular email was that the idea the author purported to own was not only not a new idea, it was a problem already being solved by existing enterprise software. The pitch was for turning existing functionalities into an SME level product. That’s what we call “an execution play,” in investor lingo. It means the idea is the market, not the product.

You should know this if you’ve ever been to a pitching event with a Q/A. There’s always a smarty-pants judge who points out he’s heard every idea before. Most of them have, it’s just that lazy judges say that instead of something more useful. We’ve all heard the ideas before. There’s nothing new under the sun.

That’s ok because we don’t care much about ideas. We care about finding big problems to solve, because that is going to determine how successful your company is. The thing about big problems is that everyone knows about them. If they didn’t know about them, they wouldn’t be problems to begin with.

So our biggest problems with picking startups is finding the right team to solve that problem, and doing it at the right time.

Just think about this logically for a minute: you have an idea, and it’s a pretty good one. Genius in fact. What industry is it in? How big of a problem does it address? How many people work in that industry? How many people are customers or users of the products of that industry?

Even if we’ve never heard an idea before, it usually takes about 30 seconds of googling to figure out it isn’t a new idea. Even if we can’t figure that out, one of our alumni or mentors can, and frequently do. The question is not whether an idea is new, but whether the problem being solved is real.

The bigger the problem you’re solving is, the higher the likelihood that somebody, somewhere (and more likely many people, everywhere), have had the same exact thought. Their description of it might be different, and their way of fixing it might be different, but the idea is effectively the same.

We choose startups based on their vision, and how that vision makes sense for that team, that technology, and the problem they want to solve. It is mostly about people.

To someone not familiar with our thinking, it might look like we hear ideas, then “give them” to our startups. But, thats pretty misleading. It would be like accusing a filmmaker of watching other films, or being inspired by literature. Ideas are wonderful and sometimes very clever. They are just never really entirely new. If they were, they wouldn’t make sense when you heard them.

Of course the iPhone would have been a truly new idea before the invention of electronics. But then, nobody ever had any reason to imagine such a thing before the discovery of electricity, let alone computing and the million other nested inventions in a smartphone. Inventions are always a blend of established knowledge with new approaches.

This popular phenomenon of “idea theft” is more pronounced today in the tech industry than in almost any other- and it’s particularly true in products that rely on a simple central value proposition that is easy to copy. Many products can “do the same thing,” but very few can do it in just the right way.

Look at Facebook, and the endless accusations of their “stealing,” the Stories idea from Snapchat. It’s true that Facebook recognized an opportunity when it presented itself, but the idea of using media to create a narrative was invented in the past few years is ludicrous. Do we accuse Uber of stealing the idea of a livery service?

One of my favorite ever blog posts about this topic is from the creator of the game 3s. When I first read this piece when it was published, I was a fan of their copycat competitor, 2048. Since then, I’ve adopted 3s and actually played it on a near-daily basis for the past 3+ years. Today I understand the piece very differently. What I saw then as mostly whining about competition, today I see as a powerful argument in favor of vision:

“We wanted players to be able to play Threes over many months, if not years (…)The branching of all these ideas can happen so fast nowadays that it seems tiny games like Threes are destined to be lost in the underbrush of copycats, me-toos and iterators. This fast, speed-up of technological and creative advances is the lay of the land here. That’s life! That’s how we get to where we’re going. Standing on each others shoulders.

We want to celebrate iteration on our ideas and ideas in general. It’s great. 2048 is a simpler, easier form of Threes that is worth investigation, but piling on top of us right when the majority of Threes players haven’t had time to understand all we’ve done with our game’s system and why we took 14 months to make it, well… that makes us sad.”

What this really is, is a startup founder talking about how simple his idea was, and how important his dedication to his craft was to the delivery of a special product. He was absolutely right to point out that comparisons between his product and the copycats were unjust, and would eventually be judged premature.

He may not have ended up with the most popular game, but he did end up with the best game, and customers paid for that game, not for the copycats (which were free). They “lost” in terms of being a market leader, but they succeeded in their vision for their users and product.

When you actually stop to think about it, it’s hard to name a lot of first movers in tech who managed to dominate their industries, or even survived. As CBinsights has pointed out using data supplied by failed startups themselves, “late to market” doesn’t even qualify in the top 20 reasons for failure.

Shockingly, being first on the market is not a powerful predictor of success. In fact, study has shown that it may be associated with a higher risk of failure. MIT Sloan Management Review noted over 20 years ago that claims of first-mover advantage among successful businesses across a broad base of industries was caused by an effect known as “Survivorship Bias.”

Survivorship Bias, a form of selection bias, occurs when we attempt to judge the relevant qualities of a group, such as a group of startups, after they have become successful, while ignoring the qualities of those who don’t make it. This can lead us to misjudge the importance of some qualities in survival, because we are not looking at all the data.

The logical error is easy to spot when you know how. If I told you that a study of billionaires shows that 75% of them wear white shirts, but only 25% wear other colors, you could conclude that having a white shirt improves your own odds of success. But you would likely be in error. The population as a whole might be 90% white shirts, meaning that in fact another color is even more correlated with success when looking at all the data.

Think about that the next time you dress a certain way because Steve Jobs did. That would be aggressively missing the point.

Survivorship bias arises when we don’t have good data on failures, obviously because they have failed. However, there are ways of determining that survivorship bias is at work. For example, the inconvenient truth that the failure rate for Silicon Valley based startups is actually *higher* than in many other regions. As the Guardian suggests in the above article, this is precisely because so many successful companies are based there. The local standards for success are higher, so failure rates rise.

Does that mean you should or shouldn’t move to Silicon Valley? I don’t know. I know it does mean that moving to Silicon Valley is not guaranteed to help you.

Want even more proof of why first to market is overrated? Of the top 10 startups according to StartupRanking.com, not a single one of them was first to market. Some, like Slack, were not even the first multi-billion dollar companies in their own category. Booking.com offered private flat rentals in the 90s, a decade before Airbnb, and Couchsurfing was founded in 2003, a full 5 years before.

A dark and terrible secret of the tech industry -just kidding, it’s obvious- is that most of the ideas that end up getting made don’t come from the founders themselves anyway. The core idea is there, but the final product with market fit is usually a distant cousin of the prototype- the work of many minds.

Where do most actionable ideas come from? Users, customers, advisors, investors, partners, friends, family, and hatemail. I’m only sort of kidding on that last one. The point is that startup founders generally start with wanting to solve a somewhat unclear problem in a somewhat unclear way. They attend accelerators and get early users, investors, and corporate partners on-board to help them make the problem and the solution more clear and actionable.

The really successful founders are not idea machines, they are execution machines. They know how to listen, recognize a good idea when they hear one, make it work, observe the results, and adapt further. There is great creativity and invention in this process, but it is not about ideas, it is about empathy, passion, and skill.

Now that I’ve ruined your beautiful vision of the perfect idea that will make you rich, I will give you a moment to thank me.

You should be happy after all: now you can get on to the stuff that really matters, like building a company you can be proud of, that provides something your customers really value.

Here’s another reason you should be celebrating: you can work on anything you want to. Somebody else already tried it? Not like you will. The problem is already solved by somebody else? I bet some of their customers aren’t happy.

Oh and nobody can credibly accuse you of “stealing their idea,” since ideas are not automatically intellectual property. Intellectual property is the work product of an idea, not the idea itself. Copyright applies to words and images and code. Patents require you to actually design an invention and describe how it works in detail; even then, it’s not automatic. A patent is for the bread slicer, not the sliced bread.

Call the lawyers. We’ve got a live one.

If someone has already done what you want to do, thank God somebody has already proven you can make money in this field- that makes your job a lot easier. Or thank goodness somebody else tried this and failed. Now you know not to make those same mistakes. See? Now that ideas don’t matter, the world is truly your oyster. Go forth and start up.

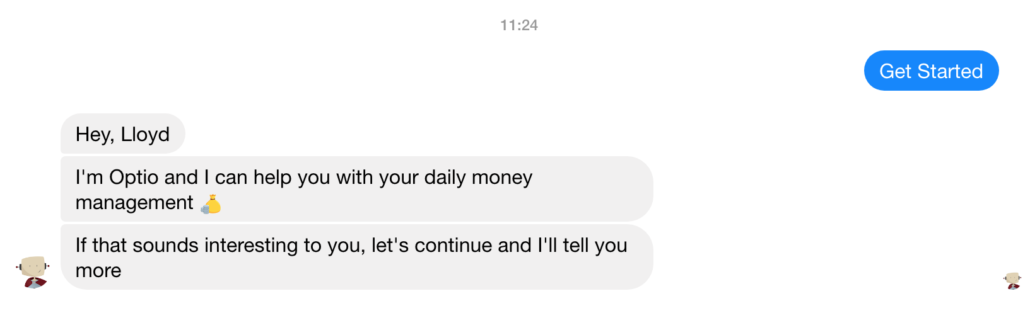

Last month we announced that OptioAI, a member of StartupYard Batch 8 and StartupYard’s first Georgian startup, had joined TechStars Berlin. Techstars is the world’s largest accelerator network, with over 1000 invested companies, and $3.3bn raised over the past 12 years. OptioAI is through the first month of the program already, and will present at the Berlin DemoDay on April 19th.

OptioAI joined StartupYard with a plan to create a text-based finance management platform for millennials who weren’t seduced by traditional banking (which is to say, most of them). Today their core mission remains the same, and has evolved to become a text-based platform that “makes your money talk to you,” by connecting users with their financial data in a natural way, via voice and chat.

I checked in with Shota Giorgobiani, Co-Founder and CEO at Optio, to find out how the Techstars program is going. Here is what he had to say, this time via email.

The funny thing is, applying to TechStars started more as an experiment.

We’d heard how hard was to get to Techstars. Techstars does not officially publish information about the number of applications they get for every batch, but rumors say that only 1-2% of initial applicants get to Techstars and the number of applications per program can be near 1000.

Furthermore, Techstars generally accepts only 1 or 2 early stage company per batch, so it looked almost impossible right from the beginning. Our goal was to understand how the process works and prepare for the future when we would be “ready,” but as always, you never know when you are “ready” and what “readiness” means. So we ended up by being selected for Techstars Berlin, which actually is a great outcome of the “experiment!”

The first part of the selection is pretty much standard: you send your application, you are shortlisted and then have a Skype call. If you are in the final round, you are invited to selection day.

Some cities have 2 meetings with startups and some just one, but overall it’s the same as at StartupYard. The main difference is the final selection process: It’s not like a “traditional pitch” competition, or a series of one-to-ones, it’s more a face to face meeting with the whole selection committee.

We had 2 meetings, each for 15 minutes with 2 different groups. The idea of this meeting for Techstars team is to get to know the team. It’s a known fact (and it’s true not only for Techstars) that most of the time, especially early-stage startups are chosen because of the team, not because of the idea or product. And when I mention team, not only the credibility of the team is important (like how many years have you been in the industry), but also if the team can be managed and helped to make better decisions or not.

This was something we really improved on at StartupYard: how to listen and to show that you are taking questions seriously; how to engage with debate and not be defensive.

Also very important is to show what you have. No matter if it’s a working product with 1000+ users or mockups of your idea. You should be excited about what you are doing and you should naturally show this excitement. It’s even good to start your talk with the demo (and most of the time – you are asked to do so).

One last thing: 15 minutes is too short period to cover everything. You may be tempted to use up your time talking about your plans, but you should be able to cover most important topics in 2-3 minutes and move to the Q/A part, where you have a chance to show your competence, passion, vision and also show where Techstars can help you. So you should be prepared and be able to manage your time well.

For us, it was a little challenge, because we naturally tend to speak a lot about our company, and you should really train yourself to do it quickly. At the end of the day, it’s all about the match: a personal match between team and Techstars and clear view of how Techstars can help, if any of these is missing, I think you will not be accepted.

I can talk about that for hours, but to be short and clear: I think, based on our current stage, we had little chance to get to Techstars, if we had not been in StartupYard.

There are clear reasons for that: at StartupYard we learned to describe what we do and who we are quickly and clearly. This is a crucial thing, you should be able to explain in 2-3 mins why are you building the company, what are you building, how this team can achieve the goal and etc. And that’s very hard to do, it takes time and practice. Second is credibility: I think it’s very hard to get into the world’s top accelerator just by sending the application. Sure you can, but for us, at such an early stage and being from Georgia, it feels impossible.

Your network is your key to the world! You have to always be building it up and making it stronger.

For example, our story with Techstars actually started in Prague, in StartupYard, where we meet Techstars Berlin MD, Rob Johnson, and had the opportunity to talk with him and tell what we were doing. Rob was there because of StartupYard, so already you can see the network effect.

Rob suggested we try and apply for the upcoming program. When someone tells you that, listen to them! That’s a shortcut to being noticed among hundreds of applicants, because it comes from within their network. It comes with a degree of trust and confidence.

And believe me, if you are not already generating revenue and growing steadily and are still proving that your product makes sense, such a “shortcut” can be your only chance.

Overall, StartupYard gave us a lot of direct knowledge and experience and maybe even more importantly, wisdom, which helps us every day at Techstars.

For example, after one bloody month of mentorship in Prague, we had a very clear understanding of how the process looks and feels, how to prepare for meetings, what to expect from mentors, etc. Having that experience is invaluable when you get to Techstars and it helps you get the most out of the mentors there.

The main challenges now are achieving strong product-market fit and finding a sustainable business model.

So far we have not changed our strategy overall, but that’s an ongoing process and considering the stage of our company, there can and will be changes. For now, we are still working to give millennials an easy way of managing their money through conversational interfaces. At the end of the program, we want to have good traction in terms of users, the finalized core of the product, a clear vision of our business model and 1 or 2 pilots with potential B2B customers. That’s the plan for now.

Yes, we just released an updated version and lots of changes are ahead.

We decided to focus on the simple, yet very valuable functionality of the product, so we narrowed down our long list of the feature set to something, we believe is valuable for our users on a daily basis. Still, we have to do lots of experiments and see how it goes, but we are now more solid in short-term vision and plan.

In short, we want to create a super simple tool/routine for our users, that can help them with daily money management. No long-term savings goals, no 5-year plans of repaying your mortgage – we are focusing on daily money management. Sounds simple, but as usual, the devil is in the details: if you can’t manage your daily spending, there’s no chance to solve your long-term problems., So for now, that’s our main focus and strategy.

This is going to be a post about what makes startups fail. But first of all, if you don’t regularly read CBinsights and receive their newsletters, then stop reading this post and go sign up. There’s a reason most newsletters don’t have 400,000 weekly readers.

If you do, then you may have seen a bit of content that CB insights has been updating consistently since 2014: The Top 20 Reasons Startups Fail. This is a list compiled from a sample of over 100 “Post-mortems,” written by founders and employees of high profile startups that failed.

The list is ranked by the number of times a specific reason for failure is cited – each post-mortem contains some combination of these reasons:

We won’t detract from this piece by hashing out every reason startups might fail. Instead, we’re going to focus on 3 of these reasons, and how to avoid letting them kill your startup before it starts.

Some of these reasons also explain why we choose not to work with some startups that apply to our program. If you’re thinking about applying to an accelerator or talking to early-stage investors, then these are important questions to ask about yourself and your business.

Oh boy. This is a big one. For me, this is the big one. The mistake that kills a startup dead like a beautiful rose in a dry vase. Ignoring your customers, refusing to think about them and to be driven by their needs, is the kiss of death.

It all starts so innocently: a humble coder working nights and weekends on a passion project. That’s the way a startup should start, but the nature of a startup is to grow – not just in size but in mentality.

Every startup investor and mentor has had this conversation:

Mentor: who are your customers.

Founder: Well we are our own customers.

Mentor: Yeah… but who is going to be your customer? What do they need?

Founder: They need our product.

Mentor: Why?

Founder: Because it’s awesome. They’ll love it.

Mentor: Yeah but… why your product? What not a competitor?

Founder: Because we are newer/smarter/cheaper/better UX, etc.

Mentor: How do you know that’s what they’re looking for?

Founder: Because we are the customer.

Points to you if you can spot the tautology in this reasoning. I strongly agree that a problem you are passionate about solving has to be one that affects you. In that sense, you should be your first user, you just need to remember that the customer is somebody you can also learn from.

A good way of remembering that is this: you didn’t buy your product. You built it. Your customer will buy it. Even if you both have the same problem, you are not the same person.

Again, it’s essential to create something you would use yourself. It just isn’t enough. Great products involve a deep insight into the motivations of customers; even when that insight is a very simple one, or an instinctual one, it does not come about by chance, but by observation and curiosity about people.

Thinking About Your Customers:

How to avoid this one? It happens that we’ve shared a lot of content on this theme. Positioning for Startups, Bulding a Killer Customer Persona, and The “We” Problem, are good places to start.

In short, it comes down to having a process. Here is one you can try:

There’s not one way to do this, but there are plenty of ways to do it poorly. Not having a clear idea of what you know and don’t know about customers is a mistake that’s easy to avoid. Paul Graham put it this way in one seminal blog post:

“When designing for other people you have to be empirical. You can no longer guess what will work; you have to find users and measure their responses.” -Paul Graham

“You need passion,” we are so often told. Less often are we told what that means.

I think this is why some founders confuse “having passion,” with “being energetic,” or “assertive,” or “dominant.” These are not the same things.

Passion comes from within – it’s not a performance art; it guides what you say but also how you think, what you are willing to do, and what setbacks you are willing to accept. In short, it’s not about how you behave, but about who you really are.

Everyone has some passion. It’s the thing that keeps you up at night, and bothers you throughout the day. A little voice in your head telling you something needs to be done.

Understanding their own passion is pretty hard for some people. We’ve seen that a lot. We spend a lot of time with founders trying to find out what gets them really engaged and excited about their work. What gets you out of bed in the morning is what’s most important in your work.

One of the first thing we ask applicants to StartupYard is: “Why are you doing this?” The answer says a lot about your passion.

A lack of passion is easy to spot, if you know what to look for. Here’s an overview of the qualities that typically tell us a founder lacks the passion they need to move forward:

Seeking your Passion: How do you know you’re doing things for the right reasons?

In my view, this is a simpler question than people often make it. We are taught from an early age that we should emulate those who are successful, but education systems often don’t help us to really understand why successful people are special to begin with: because they have a passion for what they do.

For all the tactics, tricks, and habits of the rich and famous, passion underlies everything. People succeed when they do what they are good at, enjoy it, and are willing to work harder at it than anyone else.

Just consider the following questions if you want to get in touch with your true passion:

If your answer to any of these is “yes,” then you ought to think hard about what you’re doing. You haven’t yet found your passion.

“When a great team meets a lousy market, market wins. When a lousy team meets a great market, market wins. When a great team meets a great market, something special happens.” – Andy Rachleff, CEO, Wealthfront

Even if you’re doing something you really care about and you’re doing it for customers you understand really well, you can still fail to make the right product for the right market.

Andreessen-Horowitzs has a fascinating post on product market fit, in which they quote Andy Rachleff who developed the PMF framework, starting with what he calls a “Value Hypothesis:”

“A value hypothesis identifies the features you need to build, the audience that’s likely to care, and the business model required to entice a customer to buy your product. “

There are two sides to the PMF equation. Market, and Product. Missing PMF means failing to address a specific market with exactly the right product, at the right price.

Right Market

Andreessen-Horowitz heavily emphasizes finding the right market first, which is another way of saying that you must identify the right problem to solve. If you pick the wrong market, you can end up building a product that people love, but won’t pay for.

This happens more than you’d suspect: plenty of popular products have never gained good PMF. Even mega-popular products like Twitter can teeter on the edge of failure, and take over a decade to achieve PMF (which Twitter seemed to do only in 2017, with their advertising business and focus on media and news).

Other orphans of bad PMF are products like Tumblr, Vine, Soundcloud, and BetaMax tapes. Each of these has either failed, or is now on life-support. The latter example of BetaMax is included in this extensive list from Business Insider. In fact, virtually all the products in this list failed because of lack of PMF. Not because the products were bad, but because the business model didn’t work: the market didn’t sustain them.

The Right Product

“First to market seldom matters. Rather, first to product/market fit is almost always the long-term winner.” – Andy Rachleff

So picking a problem you can solve, for a market that wants a solution critical. Still, you can manage this and still fail. The product that solves that problem also has to appeal to the customer enough for them to use it.

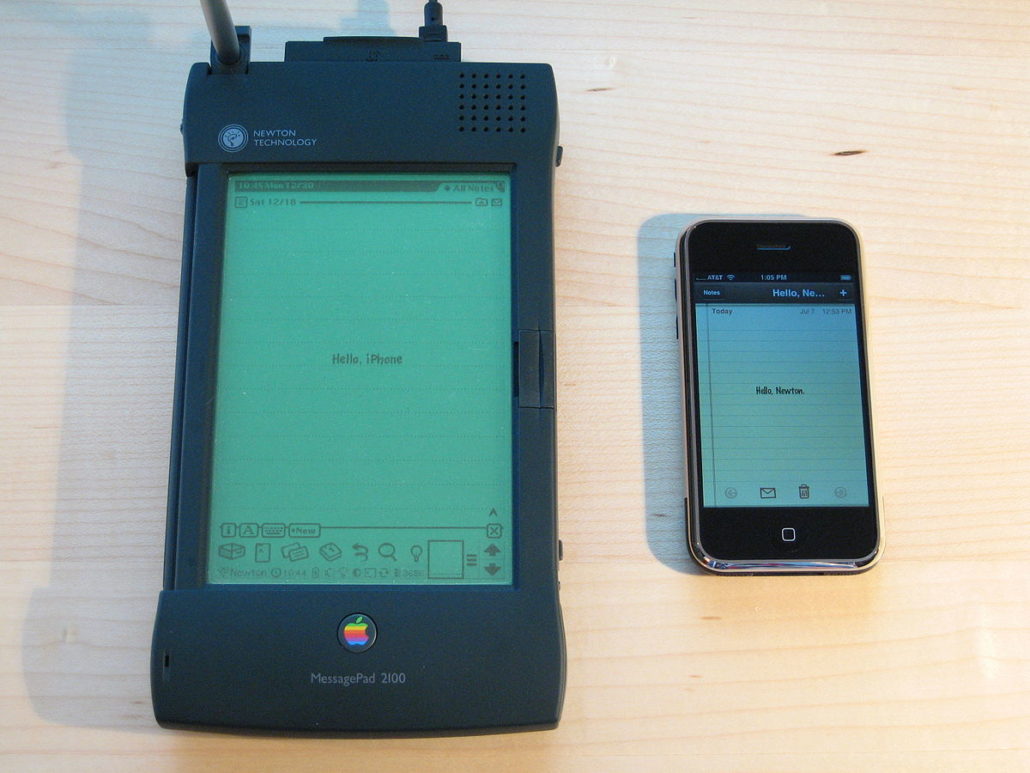

A great example of this also comes from BI’s list: The Apple Newton line, which lived from 1993 to 1997, and which Wired later called a “Prophetic Failure.” What most people don’t know about the Apple Newton line was that they very accurately predicted three distinct product categories, which would emerge in the following 15 years: the smartphone, the tablet computer, and the modern consumer laptop.

In many ways, looking at a Newton from 1995 feels like looking at a cyberpunk version of a modern device, made to look like a 90’s product.

The Newton failed in three categories that would go on to be the fastest growing market categories in history for computing, but still failed because the technology wasn’t ready. As the project lead Steve Capps said later: ““We were just way ahead of the technology. We barely got it functioning by ’93 when we started shipping it.”

The series failed at least partly because the market was not ready for such devices, but also because of its infamously bad character recognition feature. Even though later editions of the devices improved on the original, it was too late for Apple, which would spend the next 20 years rebuilding itself and slowly reintroducing all of these concepts in the form of the iPhone, iPad, and Macbook.

Testing the Value Hypothesis:

Like listening to your customers, PMF is all about trial and error. Make certain assumptions, test them with a minimum viable product, make more assumptions, and test them. The clearest milestones for PMF come from customer feedback about the Value Hypothesis.

You can begin to test this hypothesis right away, even with just an idea- with no product to show. It’s pretty simple: if you get confusion, lack of enthusiasm, or even hostility, either it’s the wrong product or the wrong market. Find out what the person you are talking to does want, and also look for others who do want the product you’re pitching. Chances are the answer is somewhere in the middle.

This is a bit like fishing. Either change the location or change the bait. It just takes time and consistency. Fish long enough, and you can get lucky.

For example, I was attending a tech conference a few months ago, when I got the chance to meet the former Senior Vice-President of a major electronics company. He mentioned that he helps early stage hardware companies find PMF, and I mentioned we had just such a company seeking PMF: Steel Mountain.

He asked me what the company did, so I gave him the 90 second water-cooler pitch. Within a few moments he was nodding. When I got into some of the features, he was saying: “yes… yes.” When I finished, he exclaimed: “I can’t believe no one has done this! When can I buy one?”

This, I must repeat, was the former Senior VP of a major electronics company, whose products you probably own. Nobody had ever pitched him this particular idea in just the right way before. That is a powerful indication of PMF. You don’t have to convince the customer they need the product, because they know they need it.

Still I may lack some important information. Is this customer representative of a distinct market segment? Is the business model workable for the target market? Does the product work the way they want and expect?

You still have to explore all those details, but enthusiasm for the product’s core value proposition is a great milestone. It was then the Steel Mountain team’s job to continue testing the product with the same customer and others like him.